Will you be setting up an HSA in 2022? I’m definitely going to, and for good reasons!

You might not think of your health insurance as being a potential avenue for tax savings. But depending on the type of plan you have, an HSA could do a whole lot more than just help cover your medical expenses.

In this post, we’re going to explore HSAs and all of the benefits of having one. I’ll also go over some tips for how you can go about setting one up.

This post may contain affiliate links. If you purchase a product or service from an affiliate link, we may receive a small commission. This supports our website and there is no additional charge to you. Thank you!

What is an HSA?

HSA stands for “health savings account”. It’s a special type of account where contributions are made and then later used to reimburse yourself for qualified medical expenses. The money you put in is tax-free, so you’ll effectively pay no taxes on most health-related items and services. To be eligible, you must be enrolled in what the IRS defines as a high-deductible health plan (HDHP).

HSAs have only been around since 2003, and so they’re a relatively new concept that’s not well known or appreciated. However, anytime the IRS gives you the chance to avoid taxes, it’s worth checking out!

How Much Can I Contribute to an HSA?

An HSA can be funded by money from you, your employer, or anyone else who wants to contribute. However, just like a 401k or IRA, there’s a limit to how much can be put into one.

The following are the HSA contribution limits for 2022 (employer and employee combined):

- Self-only: $3,650

- Family: $7,300

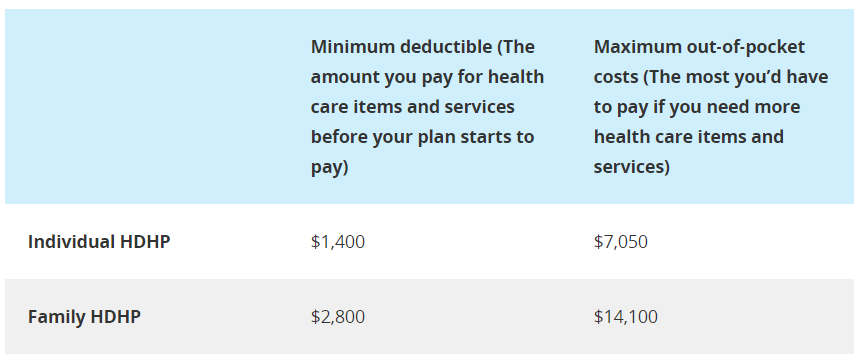

What is a High Deductible Health Plan (HDHP)?

An HDHP is a health care plan that exceeds certain deductibles and out-of-pocket costs. As of 2022, the IRS defines the minimum thresholds for an HDHP as follows:

Source: Healthcare.gov

Note that both the individual and family values have to be higher than these minimums in order for the plan to be considered as an HDHP and thus give you eligibility for an HSA.

Borrowing an example from the IRS’s website, suppose your healthcare plan has an annual deductible for individuals and families that are $1,500 and $3,500 respectively. Unfortunately, the plan wouldn’t qualify as an HDHP because the deductible for an individual family member is less than the minimum annual deductible for family coverage ($1,500 < $2,800).

What Are the Benefits of an HSA?

There’s a lot of enthusiasm out there for HSAs. Long-time personal finance blogger The Mad Fientist has hailed it as the Ultimate Retirement Account writing about its many unrealized benefits, especially for those people who want to retire early.

Others see an HSA as an opportunity to cash in on the triple-tax advantage it provides. Here’s what they mean by this.

1. HSAs Reduce Your Taxable Income

Just like contributions made to a traditional IRA or 401k, federal taxes (and most state taxes) are excluded from any income that you put into your HSA. This means your adjusted gross income or AGI (the number your tax return uses to calculate your tax bill for the year) will be lowered with every contribution.

2. HSAs Promote Tax-Free Growth

An HSA isn’t just some boring-old savings account. Similar to an IRA or 401k, your money gets invested in funds that have the potential to grow and compound over time. With each withdrawal that’s made to cover a medical expense, a portion of it will come from investment earnings that are being cashed in tax-free.

3. Potentially No or Reduced Taxes During Retirement

When you reach age 65, by design your HSA will become eligible to be converted into a traditional IRA. Depending on how much money you’ll need to cover your living expenses and your other income sources, you might potentially be in a lower tax bracket than you are now. Therefore, you could expect to pay a lower tax rate on these withdrawals.

If you’re particularly clever with your retirement plan, you might be able to get your taxable income below your standard deduction. If that happens, the money you’d be withdrawing from this converted HSA would be tax-free.

HSA vs FSA – What’s the Difference?

If some of the rules for an HSA are sounding very familiar, then you might be thinking about a similar style of plan called an FSA or “flexible spending account”. FSAs are also a useful way to set money aside tax-free and then later reimburse yourself for qualified medical expenses. However, there are some very important distinctions you should know.

1. FSAs Have a “Use It or Lose It” Policy

FSAs expire on an annual basis, so users have to be careful not to contribute too much to an FSA or they’ll forfeit any unused funds. By contrast, HSAs never expire so there are no worries about how much you put into one.

2. FSAs Don’t Have Growth Opportunity

FSAs are nothing more than a temporary holding account where your contributions will be stored until you make a reimbursement claim. Because the account bears no interest or gets invested, the money you put inside of one is never allowed to grow the same way it can with an HSA.

By contrast, money invested inside an HSA could theoretically double in as short as 7 to 8 years. This is, of course, dependent upon fund performance.

3. FSAs are Not Portable

Before you can participate in an FSA, it has to be offered by your employer. This means that once you leave your work, you won’t be allowed to contribute to that FSA any longer.

By contrast, an HSA is always yours to keep. It has portability and will follow you even if you eventually change health care plans or work for a different employer.

Can I Have Both an HSA and an FSA?

Unfortunately, no. Because both types of accounts are essentially designed to provide some form of tax relief on medical expenses, the IRS does not allow you to participate in both. From their perspective, this would be “double-dipping”.

How to Set Up an HSA

Another advantage HSAs have over FSAs is that they don’t always have to be set up through your employer. If your workplace already has a provider, then this may be the easiest way to get started. It may also help in the future if you have questions about your HSA since your HR department will already be familiar with their recommended program.

If your employer doesn’t offer health insurance or you’re considered self-employed, then you have the option to open an HSA on your own. This can be done at most financial institutions such as banks, credit unions, or even insurance companies.

As with any service, it’s always a good idea to make sure the company you’re going to work with is legit and not just some sort of scam. Healthcare.gov recommends researching potential HSA providers online using a tool like HSA Search.

You’ll need to demonstrate to the account provider that your current health care plan qualifies as an HDHP. This can easily be done by providing them with proof of your insurance such as a dated statement showing the plan deductibles.

Be sure to ask the account provider about any fees they might charge. Not all providers will have the same charges, so it pays to shop around.

When filing your tax return, don’t forget to deduct your HSA contributions. These can be reported on Form 8889.

Is an HSA Right for Everyone?

With the triple-tax advantage, there’s really not much to dislike about an HSA. However, before you go signing up for one, you’ll want to look at the big picture.

For example, I have a friend who works for a company that offers two health care plans: one with a low $500 deductible and another with a $3,500 deductible that qualifies as an HDHP. If he were to sign up for the $3,500 deductible plan and his family visited the doctor even just a few times per, then they’d have to pay that whole $3,500 out of pocket. By contrast, if he stuck with the $500 plan, then most of his costs would be covered.

Like all financial decisions, you have to look from multiple angles and weigh each of the pros and cons. If you’re in a situation like my friend, then maybe there are other financial opportunities beyond HSAs to take part in, and that’s okay. But if your healthcare plan is more like mine where there’s only one option with a high deductible, then I’d strongly encourage you to consider opening an HSA.

Reader: Would you benefit from having an HSA? Why or why not?

LEARN all that you can, BELIEVE in yourself, and take actions that allow you to GROW!

Get your FREE copy of the 5 Keys To Success Guide (click here).